Vietnam’s convenience store market: rising concentration in a leader-dominated landscape

- Apr 22

- 3 min read

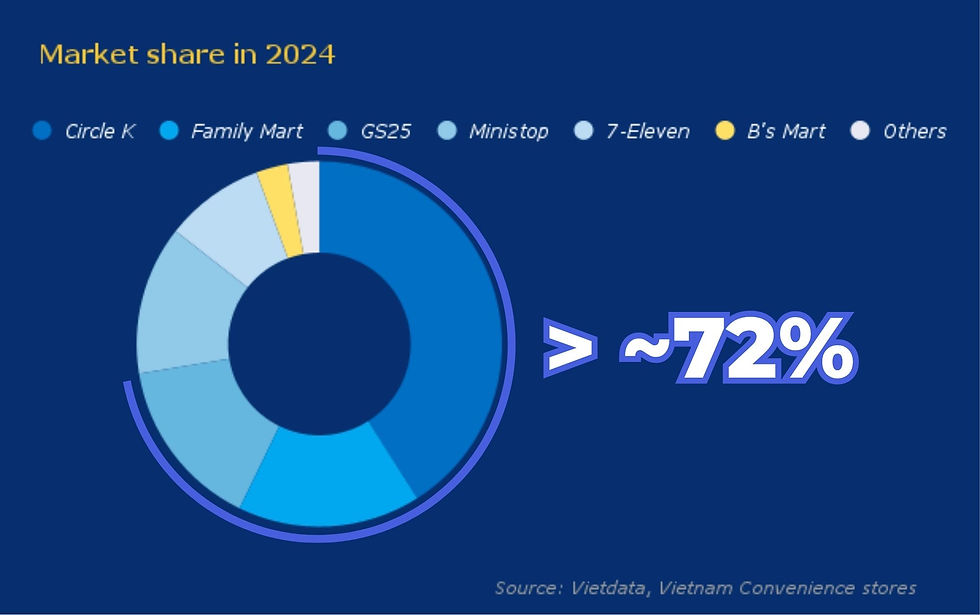

The Vietnamese convenience store market is entering a structural recalibration phase characterized by a clear “flight to quality.” Market leaders are not only preserving their scale advantages but are further widening the gap through operational efficiency optimization and enhanced customer experience. As a result, market concentration remains elevated, with over 72% of total revenue controlled by the top three players (Circle K, GS25, FamilyMart).

Source: Vietdata – Vietnam Convenience stores Report

[EN] VIETNAM CONVENIENCE STORES REPORT 04/2025 (OUTLOOK TO 2029)

$699.00

Buy Now

Circle K

Circle K continues to solidify its market leadership, capturing 41.0% of revenue share in 2024, despite a decline in outlet share from 40.3% in 2021 to 36.9%. This divergence reflects a deliberate portfolio rationalization strategy centered on “quality over quantity,” involving the pruning of underperforming stores and a strategic pivot toward high-traffic locations.

By leveraging its 24/7 operating model and a high-margin ready-to-eat (RTE) product mix, Circle K has achieved superior revenue per store relative to the industry average. Notably, the appointment of new CEO TC Cheng, alongside the roadmap to scale up to 1,000 stores by 2025, signals a transition into a phase of selective expansion, prioritizing profitability and operational efficiency over pure footprint growth.

FamilyMart

During the 2021–2024 period, FamilyMart underwent a defensive repositioning. Its outlet share declined from 15.4% to 12.5%, accompanied by an adjustment in revenue share to 16.2%. Nevertheless, the chain continues to maintain a relatively strong revenue conversion per store.

Accordingly, FamilyMart remains the second-largest player by revenue, supported by asset portfolio optimization and a focus on a target customer segment with higher willingness to pay for Japanese-standard products. Furthermore, in March 2025, FamilyMart partnered with FPT to integrate AI into its operations, underscoring its commitment to enhancing customer experience—an increasingly critical differentiator as competition shifts toward a “quality-first” paradigm.

GS25

Between 2021 and 2023, GS25 recorded hyper-growth in revenue share, surging from 3.3% to 15.2%. This expansion was driven by an aggressive land-grab strategy, leveraging a franchise model and financial support mechanisms from credit institutions (including a recent financing package from HDBank).

However, in 2024, despite continued expansion in outlet share, GS25’s revenue share plateaued at 15.2%. Amid weakening domestic consumption influenced by macroeconomic headwinds, the chain appears to be facing challenges in increasing average ticket size.

In early 2025, GS25 launched six new stores in Hanoi, marking the beginning of its northward expansion. This move reflects a strategic pivot toward deeper market penetration, while simultaneously introducing the challenge of balancing growth with profitability.

Ministop

Ministop has been experiencing a gradual erosion in relative market share (declining from approximately 15% to 13.2% over the 2021–2024 period), primarily due to intensifying competitive pressure from aggressively expanding chains, which has diluted the share of slower-growing players.

Additionally, its operating model is heavily reliant on dine-in ready-to-eat offerings—while this represents a key differentiator, it also constrains scalability compared to more standardized store formats. Meanwhile, competitors are strengthening their positioning through “lifestyle branding” (GS25) or network optimization (Circle K), thereby narrowing Ministop’s F&B differentiation advantage.

7-Eleven

7-Eleven has pursued a measured yet sustainable growth strategy, with revenue share gradually increasing from 5.9% in 2020 to 8.8% in 2024. While maintaining steady top-line growth, its unit economics remain under pressure during the accelerated expansion phase. As of 2024, the chain accounts for 9.1% of total outlets but contributes only 8.8% of total industry revenue.

Similar to GS25, 7-Eleven’s planned entry into the Hanoi market in early 2025 represents a strategic inflection point. After eight years of consolidating its position in Southern Vietnam, expansion into the capital unlocks a substantial total addressable market (TAM), serving as a key catalyst for surpassing the 10% revenue market share threshold in the next financial cycle.

Source: Vietdata – Vietnam Convenience stores Report

This page has a clean structure and easy flow for readers. I visited Online Browser Game and discovered instant play games, casual gaming options, and simple browser entertainment that does not require installation.